Why Your Salary "Finishes" Before Month End

The salary hits your account on the 25th. By the 5th, a third of it is gone and you can account for maybe half of that. By the 15th, you're doing arithmetic in your head at every POS terminal. By the 20th, you've stopped checking the balance entirely.

Then the cycle resets. The next salary arrives. The relief lasts about 72 hours.

If this is your month, every month, the natural conclusion is that you don't earn enough. Or that you're bad with money. Or both. We hear this from Delight users constantly, across every income bracket, from ₦100,000 earners in Benin City to ₦800,000 earners in Lekki. The language is always the same: my salary just finishes.

But when we actually map where the money goes, transaction by transaction, the picture is rarely what people expect.

The Invisible Drain

The big-ticket items aren't the mystery. Rent, transport, and major bills leave obvious dents. People know when those hit. What they don't see is the other current: the dozens of small transactions that individually seem harmless and collectively do the real damage.

₦1,800 for a shawarma at lunch because cooking felt like too much effort. ₦3,500 on an Uber because the bus queue was insane. ₦2,000 airtime top-up, the third one this week. ₦5,000 transferred to a friend who'll definitely pay it back. ₦4,500 on a shirt from that Instagram vendor. None of these feel significant. All of them together can total ₦40,000 to ₦70,000 a month.

That's not a spending problem. That's a visibility problem. The money isn't wasted; each purchase made sense at the moment it happened. The problem is that no purchase knew about the others. Each one existed in isolation, against a single declining balance that provides no context.

The Balance Lie

Here's what a bank balance tells you: how much money is in your account right now.

Here's what it doesn't tell you: how much of that money is already spoken for.

If your balance says ₦85,000 on the 10th, that feels like ₦85,000 of available money. But if rent is due as a lump sum next quarter and you need ₦50,000 more saved toward it, and next week's transport will cost ₦12,000, and your data subscription renews in three days for ₦6,000, your actual available money is ₦17,000.

The gap between the balance and the real number is where salaries "finish." People spend against the visible balance, not against their actual commitments. The money was never free. It just looked free.

Why Tracking Doesn't Fix This

The standard advice is to track your expenses. Write down everything you spend. Use a spreadsheet. Review it weekly.

Tracking is an autopsy. It tells you what already happened. It's useful for understanding patterns, but it does nothing to prevent the spending in the first place. You still see ₦85,000 in the account, you still feel like you can afford the ₦4,500 shirt, and by the time you sit down to review your spreadsheet on Sunday, the money is already gone.

The deeper issue is that tracking requires effort that competes with life. Two weeks in, the spreadsheet stops getting updated. By week three, you've forgotten what half the transactions were for. By month two, you've abandoned it entirely and the guilt is worse than before.

The tool that solves this problem can't live after the spending. It has to live before it.

What "Before" Looks Like

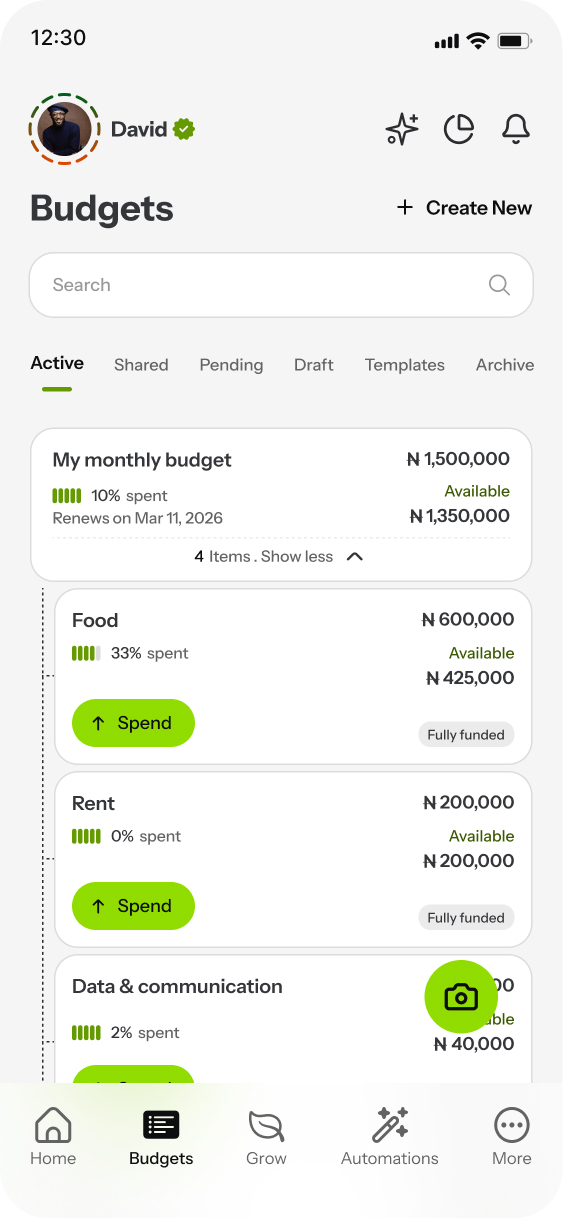

Before means every naira has a destination before it's spent. Not a vague plan. A specific allocation.

When your salary arrives, it flows into budgets: ₦50,000 to the rent fund, ₦40,000 to food, ₦25,000 to transport, ₦14,000 to electricity and data, ₦10,000 to family, and so on. The remaining amount, whatever it is, goes into a personal or discretionary budget. That's the money that's actually available.

Now when you're standing at the POS, the question changes. It's no longer "can I afford this?" based on a single bank balance. It's "does my food budget have ₦4,500 left?" or "is this coming from personal or from transport?"

The purchases don't change overnight. But the awareness does. And awareness, consistently applied, is what bends the spending curve.

The System Does the Remembering

The reason budgets on paper fail isn't that the principle is wrong. It's that paper can't follow you through the day.

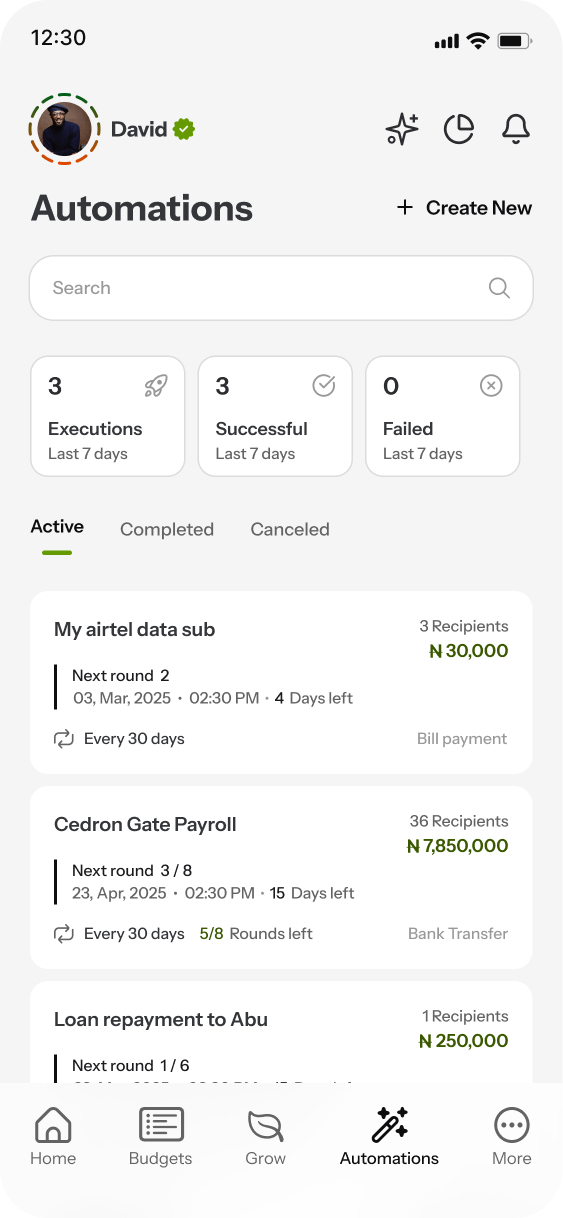

Delight solves this in a specific way. Your budgets persist: set them up once and they reset each month. Turn on autofunding and your salary distributes into those budgets automatically, in the priority order you chose. Recurring bills get automated (electricity, data subscriptions, family transfers) so the money leaves on schedule without occupying mental space.

And because every purchase runs through the app, from a specific budget, the tracking happens at the source. No manual logging. No Sunday spreadsheet review. When your food budget shows ₦8,200 remaining on a Wednesday, that's not an approximation. That's the number.

The salary doesn't "finish" any less; it's still ₦200,000 in a city that costs more than ₦200,000. But it finishes visibly, intentionally, with a trail you can read and adjust. That's a fundamentally different experience from watching a balance drain into mystery.

The Shift

There's a moment that Delight users describe consistently. It usually happens around the second or third month of using the system. The salary arrives. The autofunding distributes it. The user glances at their budgets and knows, without doing any math, without opening a spreadsheet, without the 15th-of-the-month dread, exactly where they stand.

The salary is the same. The city is the same. The obligations are the same. But the feeling is completely different.

That's what a system gives you. Not more money. Not more discipline. Just the answer to the question that haunts every Nigerian salary earner: where is it all going?

When you can see the answer in real time, the panic stops. What replaces it is a plan you can actually follow, not because you're suddenly disciplined, but because the system makes the right thing easier than the wrong thing.

Ready to take control of your money?

Download Delight Finance and create your first spendable budget in under 2 minutes.

Get Started — It's Free