Why "Saving What's Left" Will Never Work

The most common financial plan in Nigeria isn't a plan at all. It's a hope: spend what you need to spend, and save whatever's left at the end of the month.

It sounds sensible. It's the advice parents give, the approach friends describe, the default for anyone who hasn't been taught an alternative. And it almost never works. Not because people are reckless. Because "what's left" is a number that approaches zero in almost every scenario.

The Leftover That Never Appears

Here's how the month typically unfolds for someone earning ₦300,000.

Salary lands on the 25th. Rent contribution, transport, and data leave within the first week, maybe ₦100,000. Food spending runs at ₦2,000 to ₦4,000 a day. A friend's birthday. A family request. A POS purchase you don't fully remember by Thursday. By mid-month, the balance is ₦70,000 and there are 12 days to go.

The ₦70,000 isn't savings. It's the money that still has to cover food, transport, and anything else the last two weeks throw at you. By the 28th, the balance is ₦4,000 or ₦7,000. The "leftover" for savings is functionally nothing.

This happens at ₦100,000. It happens at ₦300,000. We've seen it happen at ₦1,000,000. The amount changes; the pattern doesn't. Spending expands to fill the available balance because the balance presents all remaining money as available, even when it isn't.

Parkinson's Law of Money

There's a well-known principle in productivity: work expands to fill the time available for its completion. Money obeys the same law. Spending expands to fill the balance available for its consumption.

This isn't a character flaw. It's a design flaw, in the system, not the person.

When you see ₦180,000 in your bank account on the 8th, your brain processes that as ₦180,000 of available money. It doesn't subtract the ₦50,000 you still need for rent savings, or the ₦25,000 earmarked for transport, or the ₦12,000 for data. It sees a number and makes spending decisions against that number.

The only way to break this is to make the balance lie less. To make the money that's already committed invisible, or at least, to make it clearly assigned before it can be spent.

Allocate First. Save First. Spend From What Remains.

The fix is a reversal. Instead of spending first and saving the leftover, you save first and spend the leftover.

This is not a new idea. It's the oldest piece of financial advice in existence: "pay yourself first." The problem has never been the principle. It's been the execution.

"Pay yourself first" requires you to move money into savings the moment it arrives, before you spend on anything. In practice, most people set a vague intention ("I'll save ₦30,000 this month"), then life intervenes, and the transfer never happens, or it happens and gets reversed a week later when a bill hits.

The principle needs a system. Not willpower, not reminders, not guilt. A system that executes the allocation before the person has to make a decision.

What Allocation-First Looks Like

Same ₦300,000 salary. But this time, before a single naira is spent, the money is distributed:

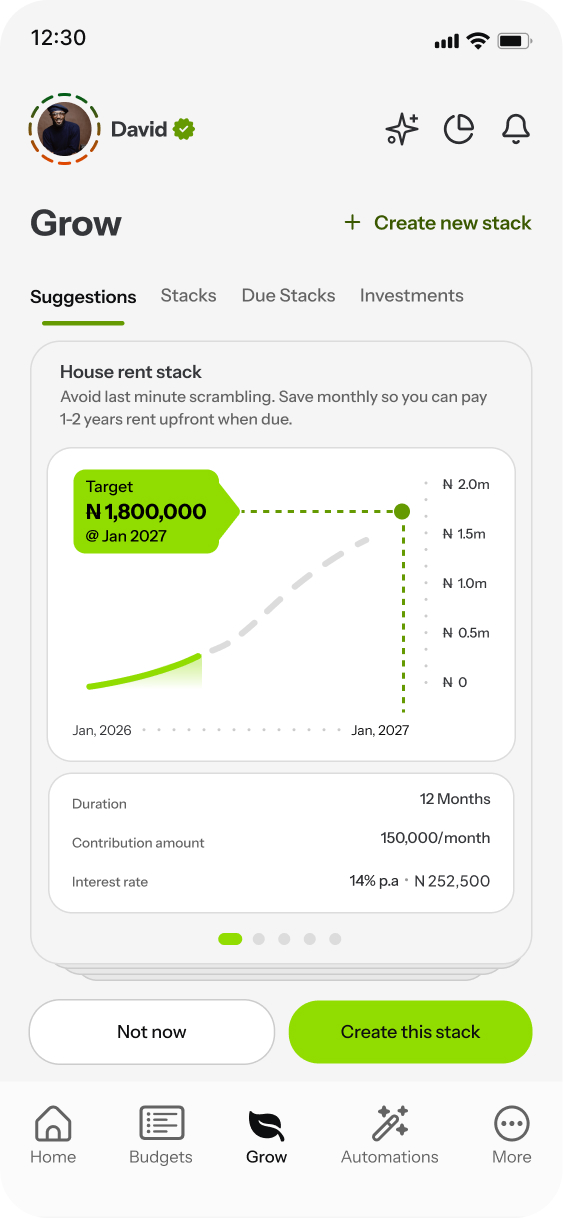

Rent Stack: ₦60,000. Accumulating toward the annual ₦720,000. Locked. Growing every month.

Savings Stack: ₦30,000. Emergency fund or a goal: a laptop, a course, a relocation fund. Untouched until the target is hit.

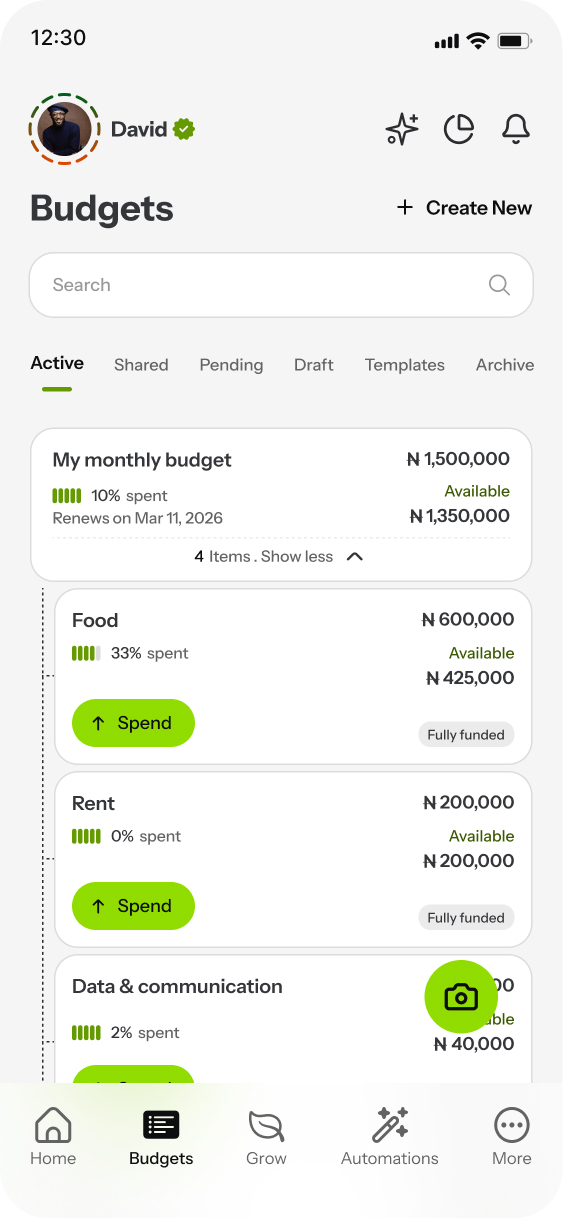

Food: ₦45,000. This is the spending boundary for the month.

Transport: ₦30,000.

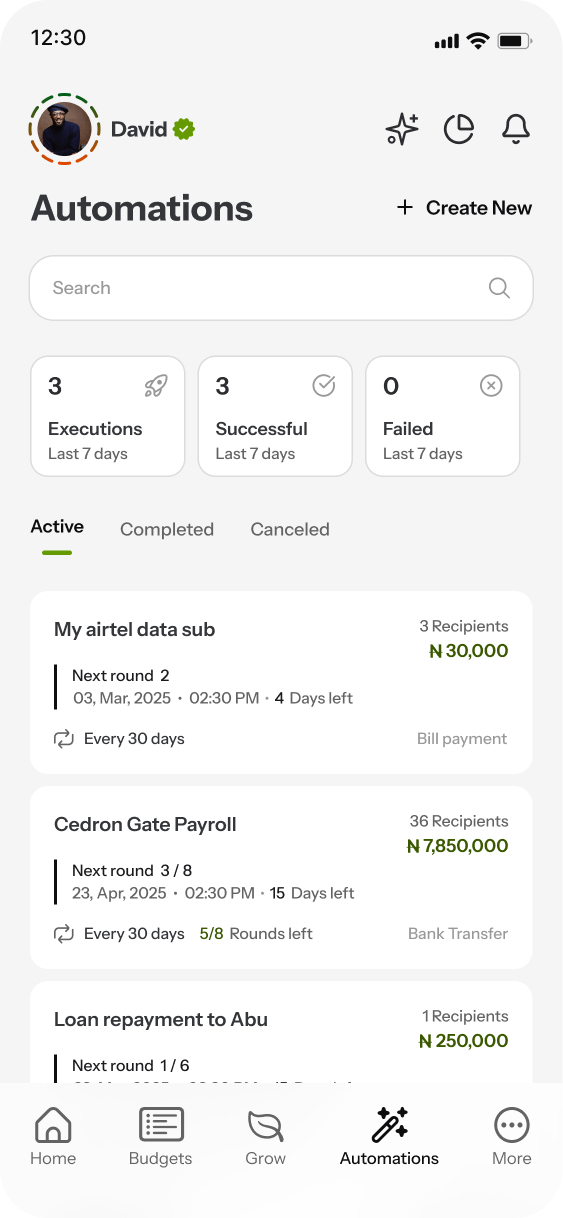

Electricity & data: ₦15,000. Automated; leaves the budget on schedule.

Family: ₦15,000. Automated to the recipients on the 1st.

Personal/discretionary: ₦105,000. Everything else. Social life, clothing, unexpected expenses, breathing room.

Total: ₦300,000. Savings didn't come from what was left. Savings came first; the spending was built around what remained after the commitment was honoured.

The ₦105,000 personal budget is still generous. But it's a bounded generosity. The person can spend freely within it without endangering rent, savings, or food. That's the key psychological shift: freedom within a boundary is more sustainable than restriction across the board.

Why Stacks Change the Equation

The reason "pay yourself first" fails in practice is that savings sitting in the same account as spending money is savings in name only. It's still visible. It's still accessible. And when the balance dips and the month isn't over, the brain treats it as available.

Stacks solve this by separating the money from the spending flow. Money in a Stack is accumulating toward a specific goal: rent, an emergency fund, a car down payment. It's visible, but it's not in the spending pool. The balance you see when you're about to buy lunch is the food budget balance, not the total account balance. The Stack money is safe because it's not competing with daily decisions.

Combined with autofunding, the entire sequence becomes automatic. Salary lands. Autofunding distributes to budgets and Stacks in priority order. Recurring payments fire on schedule. What's left in the personal budget is genuinely, honestly available. No mental subtraction required. No willpower needed.

The Reversal

Somewhere along the way, a generation of Nigerians absorbed the idea that saving is what you do with the leftovers. That it's a reward for spending carefully. That if you just had more discipline, there'd be something left.

The truth is simpler and less flattering: there will never be anything left. Not at ₦100,000, not at ₦1,000,000. The spending will always find the money if the money is available to be found.

The only way to save is to save first. Before the spending starts. Before the balance even presents itself as available. Not as an act of willpower, as an act of system design.

Set the allocation. Automate it. Spend from what remains. The leftover you've been waiting for at the end of the month? It was never coming. But the savings that arrive at the beginning of the month, those are already there, growing, before the first purchase of the cycle.

Ready to take control of your money?

Download Delight Finance and create your first spendable budget in under 2 minutes.

Get Started — It's Free