Why the 50/30/20 Rule Fails in Nigeria (And What Actually Works)

Here is the most popular piece of financial advice on the internet: take your income, spend 50% on needs, 30% on wants, and save 20%.

It sounds clean. It sounds responsible. It fits on a Post-it note. And if you earn a salary in Nigeria, it is almost certainly useless to you.

This is not to be provocative. It's simply reality. We've seen hundreds of individuals and couples try this formula. It doesn't take long to see the problem.

The Math Doesn't Math

Take a salary of ₦200,000 a month, a decent entry-to-mid-level income in Lagos. The 50/30/20 rule says ₦100,000 should cover needs.

Now list those needs. Rent contribution: ₦40,000 a month if sharing, or ₦60,000 to ₦80,000 alone (and that's modest by Lagos standards). Transport to work: ₦20,000 to ₦30,000 depending on the commute. Food: ₦30,000 to ₦50,000 cooking most meals at home. Electricity and data: ₦10,000 to ₦15,000. That's already ₦100,000, and not a single want has been purchased.

That's the first crack. In Nigeria, needs don't fit in 50%.

But there's a second crack, and it's the one nobody talks about: the 50/30/20 rule has no category for the obligations that define Nigerian financial life.

Where Does "Family" Go?

A younger sibling's school fees. The monthly contribution to ageing parents. The ₦5,000 here and ₦10,000 there when extended family calls with needs that aren't optional. Not emotionally, not culturally.

Is that a need? A want? The 50/30/20 rule has no answer because it wasn't designed for this question. It was conceived by an American senator and her daughter for a country where individual financial autonomy is the default. In Nigeria, money has never belonged entirely to the person who earned it. That's not a flaw in anyone's character. It's the reality of how families here work.

And then come the social obligations. The owambe you can't decline. The aso-ebi that costs ₦15,000. The contribution to a colleague's wedding. These aren't luxuries in the traditional sense. In many professional and social circles, they're the price of belonging.

The 50/30/20 rule treats all of this as noise. In Nigeria, it's the signal.

The Deeper Problem

The real issue isn't the percentages. They could be adjusted (60/20/20, or 70/15/15) and still miss the point. The problem is the entire approach: starting with a formula and trying to squeeze a life into it.

Formulas work when conditions are stable. A predictable income arrives on a predictable date, prices hold roughly steady month to month, and the unexpected is rare enough to be handled by an emergency fund.

That is not Lagos. That is not Abuja. That is not Nigeria. Petrol prices shift. The naira moves. NEPA decides your generator budget for you. A landlord sends a message in October: rent goes up in January. Income, for freelancers and business owners, might be ₦400,000 one month and ₦80,000 the next. No formula survives contact with this reality.

And when the formula fails, something predictable happens. People blame themselves. They conclude they're bad with money, undisciplined, unable to do what the personal finance blogs call simple. We hear this constantly: from users, from friends, from people at the very beginning of their financial journey. "I just can't stick to a budget."

Most of the time, the formula was never the problem. Applying a rigid template to a fluid life was.

What Works Instead

The approach that works, the one we built Delight around, is embarrassingly simple. No ratio. No formula. Just one principle:

Every naira gets assigned a job before it's spent.

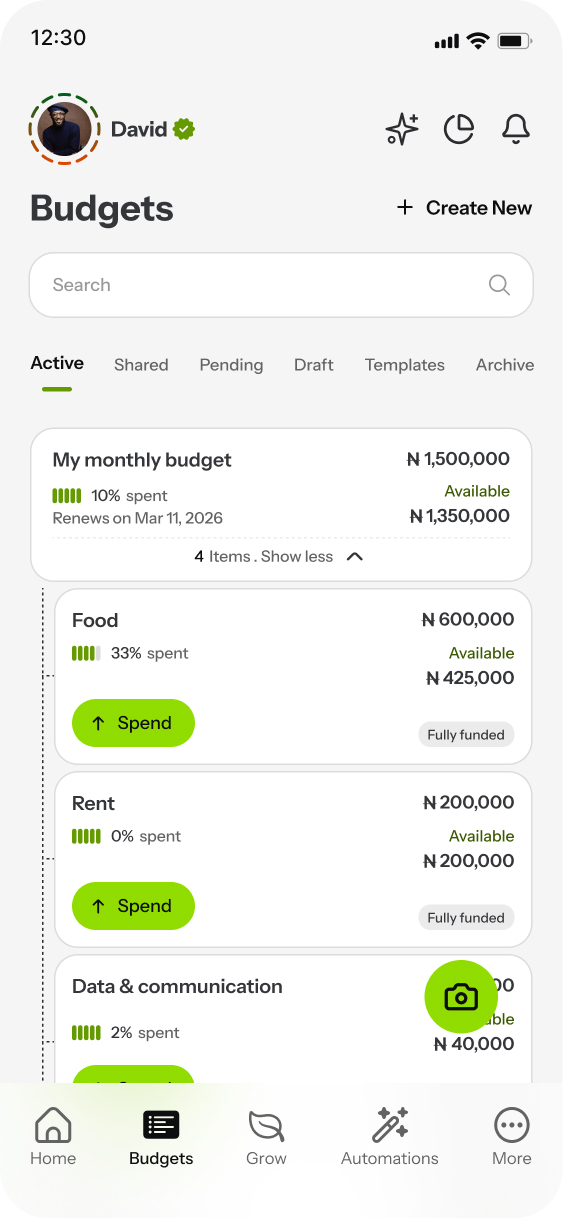

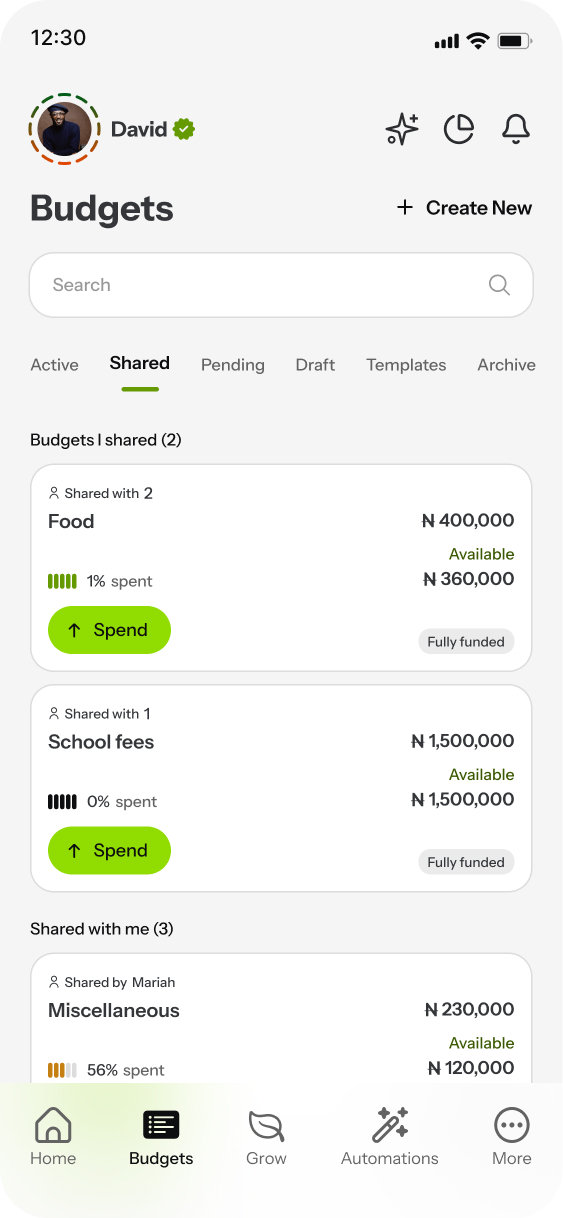

This is what we call budget-first. You create budgets that reflect your actual life (rent, food, transport, family obligations, savings, the occasional aso-ebi) and allocate your income across them. Not percentages on a pie chart. Specific amounts based on what you actually need and what you actually earn.

The difference is subtle but important. A formula tells you what percentage of your money should go where. A budget-first system asks a different question: given the money coming in and the life you're actually living, where should each naira go?

One is a rule imposed from outside. The other is a decision made from within.

How This Looks in Practice

Take that same ₦200,000 salary, but approach it budget-first.

You set up your budgets once: Rent Fund, ₦60,000 per month (because your annual rent of ₦720,000 needs to come from somewhere). Food: ₦38,000, based on what you actually spend, not what a formula prescribes. Transport: ₦25,000. Data and electricity: ₦12,000. Family support: ₦10,000. Emergency buffer: ₦10,000. Savings: ₦15,000.

That's ₦170,000 allocated. ₦30,000 remains for everything else: discretionary spending, a treat, an unexpected need.

Here's what matters: these budgets persist. They reset each month without you having to rebuild from scratch. The structure holds. You're not starting over every payday with a blank spreadsheet and good intentions. The system remembers your pattern even when life gets too busy to think about it.

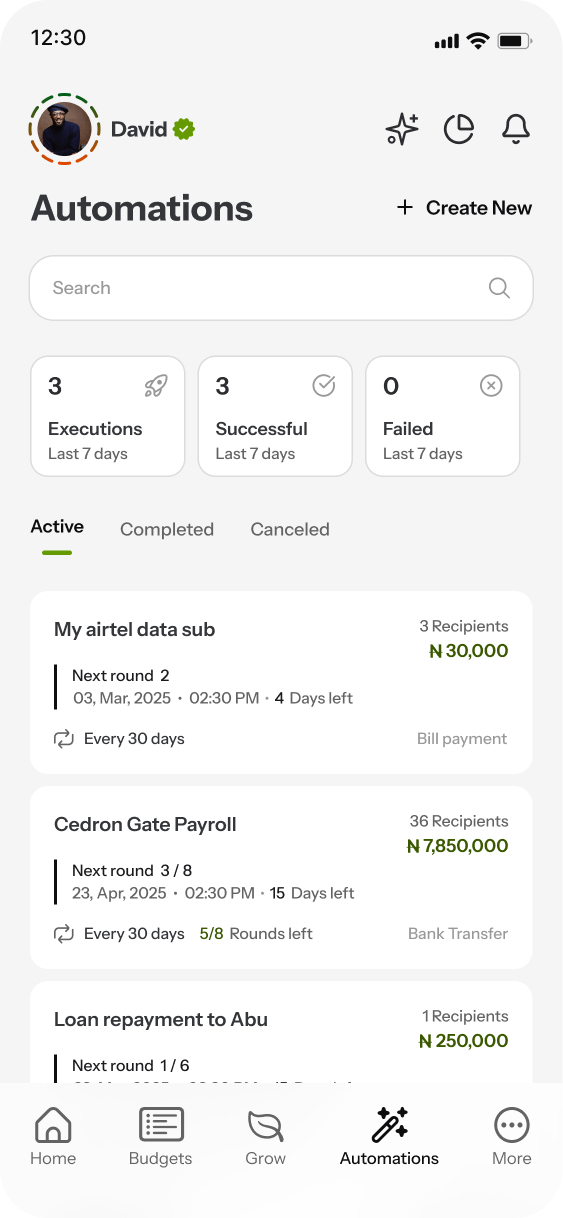

Better still, the allocation itself can be automatic. Turn on autofunding and decide the priority order (rent first, food second, transport third, savings last), and when your salary lands, the money flows into each budget in that order until it's full or the money runs out. You don't have to sit down and distribute manually. The system does what you already decided.

And when life shifts, as it always does in Nigeria, the budgets flex with it. A cousin's wedding this month? Move ₦15,000 from discretionary into a new budget for it. Transport costs jumped because of fuel prices? Adjust that budget and pull from somewhere else. The point isn't rigidity. It's awareness. Every naira that moves, moves visibly and intentionally.

Some months, the budget will look disciplined and impressive. Other months, ₦0 goes to savings because the month genuinely doesn't allow it. Both are fine. Honesty beats aspiration when it comes to money.

The Tool Matters

Budget-first is a principle. It can be done with paper and a calculator. Plenty of people start there.

But paper has a weakness: it's static. It can't autofund your rent budget the moment your salary lands. It can't tell you, at the moment of a purchase, whether the money you're about to spend has already been assigned somewhere else. It can't automatically pay your electricity bill on the 1st of every month or send your monthly family support to three different people on the same day without you touching your phone.

This is why Delight exists. It takes the budget-first principle and makes it a living system. Income gets distributed into budgets automatically, in the priority order you choose. You spend directly from the app, which means every transaction is tracked from source, without manual logging. Recurring payments are automated: schedule them once, to one or many recipients, and they happen on time, every time. The budgets reset each cycle, adapt to your pattern, and allow money to move between them when plans change, because plans always change. If a budget runs out, that's visible before the purchase, not after. If a partner is on the account, both people see the same allocations, the same adjustments, the same reality, at the same time.

It's not a tracking app that reports what happened, though it does track everything automatically. It's not a bank, though it has full banking built in. And it's not a ritual that demands your attention every month. It's a system that works with the rhythm of your life: quietly, persistently, and honestly.

Forget the Formula

The 50/30/20 rule will keep appearing in articles and Instagram infographics. People will keep sharing it. And people will keep failing at it, not because they lack discipline, but because the rule assumes a financial life that doesn't exist in Nigeria.

The alternative isn't another formula. It's a habit: sit down before the money comes, decide where it goes, and adjust when life changes the plan.

No percentages. No guilt. Just a budget that starts before the spending does.

That's the real shift. And once it happens, the question stops being "Where did my money go?" and becomes something far more useful: "Where do I want it to go next?"

Ready to take control of your money?

Download Delight Finance and create your first spendable budget in under 2 minutes.

Get Started — It's Free