How to Budget on Irregular Income Without Losing Your Mind

In January you made ₦420,000. In February, ₦110,000. March is looking like maybe ₦250,000, but two invoices are outstanding and one client has gone quiet.

This is the freelance reality in Nigeria, and it's not limited to designers and developers. Small business owners, consultants, market traders, real estate agents, content creators, and anyone working on commission lives inside this same unpredictability. The money comes in bursts. The expenses come in a steady stream. The gap between those two rhythms is where financial anxiety lives.

Every piece of budgeting advice assumes a fixed monthly salary arriving on a fixed date. When your income isn't fixed, the advice isn't just unhelpful. It's demoralizing. You can't follow a budget that requires a number you don't have yet.

But you can follow a system built for exactly this problem.

The Core Mistake: Budgeting on Your Best Month

When irregular earners try to budget, they almost always start with an optimistic number. They average their last three months, or they use a recent good month as the baseline, and they build a lifestyle around that figure.

This works perfectly, until a bad month arrives. And bad months always arrive.

The lifestyle stays. The income drops. The gap gets filled by dipping into savings, borrowing from next month's anticipated income, or running up informal debts. By the time a good month returns, it's consumed by the hole the bad month dug.

This is the cycle that traps irregular earners. Not low income; many freelancers and business owners earn more annually than their salaried friends. But the unpredictability creates a sense of perpetual financial instability that high earning alone doesn't fix.

The Fix: Budget on Your Floor

Your floor is the lowest monthly income you can reasonably expect. Not your worst month ever; that's a crisis, not a baseline. Your floor is the amount that, even when things are slow, tends to come in.

For a freelance designer earning between ₦100,000 and ₦500,000, the floor might be ₦120,000. For a small business owner whose monthly revenue swings from ₦200,000 to ₦800,000, the floor might be ₦220,000 after expenses.

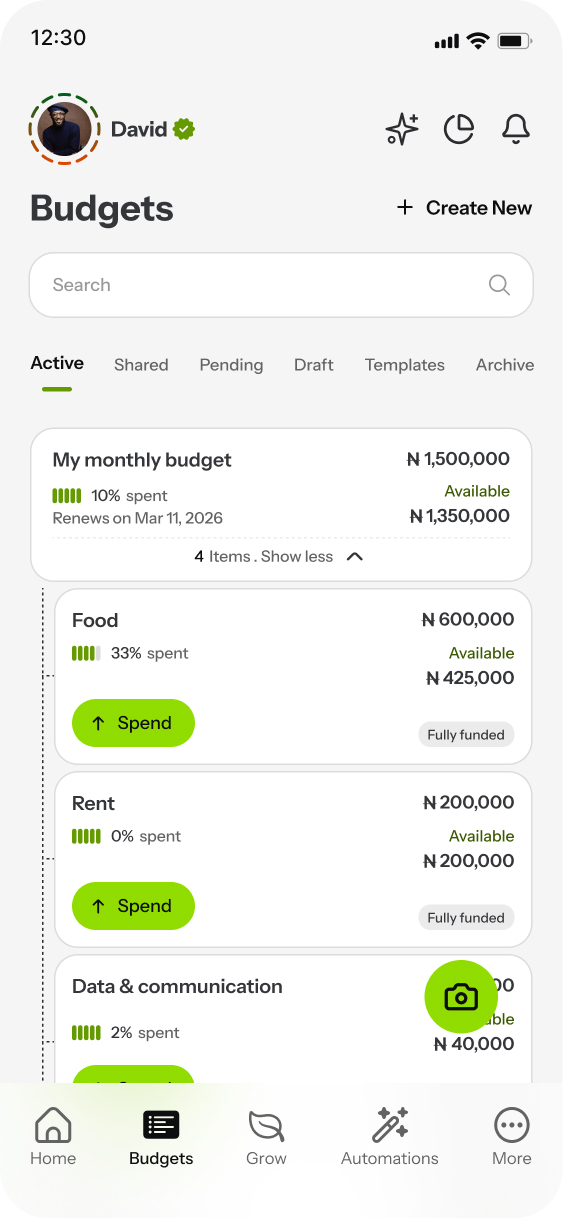

Build your essential budgets around this floor number. Not the average. Not the ceiling. The floor.

Essential budgets on the floor: Rent fund, food, transport, electricity and data, family obligations. These budgets should be fully fundable from the floor income alone. If they aren't, the floor needs to rise (more clients, higher rates, lower rent) or the essentials need to shrink. There's no formula that fixes arithmetic.

Growth budgets above the floor: Savings (Stacks), personal spending, business investment, social life. These get funded only by the income that exceeds the floor. In a ₦120,000 month, some of these get ₦0. In a ₦420,000 month, they get ₦300,000. That's not a failure in the lean month or a windfall in the good one. It's the system working exactly as designed.

The Two-Account Rhythm

The most effective pattern we've seen irregular earners use is a two-rhythm system:

Rhythm 1: Income lands. All income goes to a single receiving point. Not straight into spending. When the money arrives, whether it's an invoice payment, a sales deposit, or a commission, it lands in one place.

Rhythm 2: Monthly allocation. On the 1st of each month (or any fixed date), you allocate from whatever has accumulated. Essential budgets get funded first, in order of priority. What remains flows into growth budgets.

This creates something salaried workers take for granted: a predictable allocation cycle, even when the income feeding it is unpredictable.

In a good month, the allocation fills everything and the surplus goes to Stacks or future-month reserves. In a lean month, essentials get covered and growth budgets wait. The system doesn't break in either case. It just responds to reality.

The Surplus Problem

Here's the trap that catches even experienced freelancers: the big month.

₦420,000 lands after two months of ₦150,000. The psychological pressure to spend is enormous. You've been tight for weeks. You deserve the upgrade, the dinner, the new equipment. And you're not wrong, but the big month has a job that goes beyond this month's comfort.

The big month's real job is to fund the next lean month before it arrives.

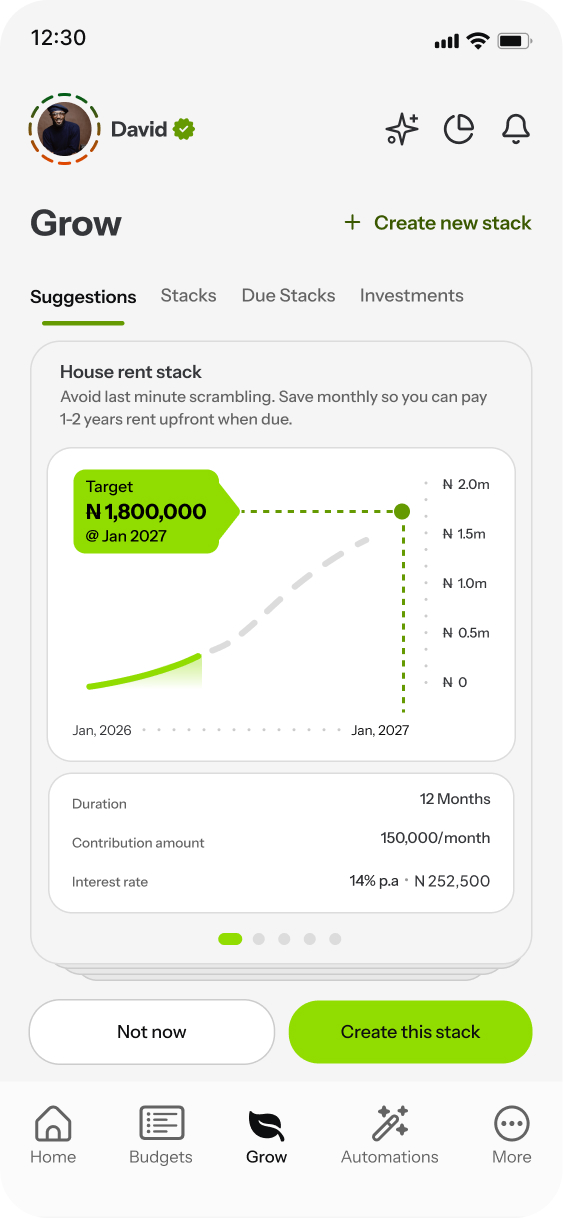

This is where Stacks become critical. A "Buffer" Stack holds one to two months of essential expenses. When a good month overfills the budget, the excess flows into the buffer. When a bad month underfills it, the buffer covers the gap. Over time, the buffer grows large enough that individual monthly income barely matters; your essential spending is insulated from the volatility.

The goal isn't to live below your means forever. It's to build a buffer that separates your lifestyle from your income cycle. Once that buffer exists, you can raise your standard of living with confidence, because you're not raising it on a single good month's hope.

How Delight Handles Variable Income

The system Delight provides is built for this rhythm. Autofunding distributes incoming money into budgets by priority: essentials first, growth second. If ₦120,000 arrives, essentials fill and growth waits. If ₦420,000 arrives, everything fills and the overflow moves to your Buffer Stack or a future goal.

You set the hierarchy once. Rent fund fills at priority 1. Food at priority 2. Transport at 3. When money flows in, it follows the order. No decision fatigue. No monthly sit-down wondering what to fund first.

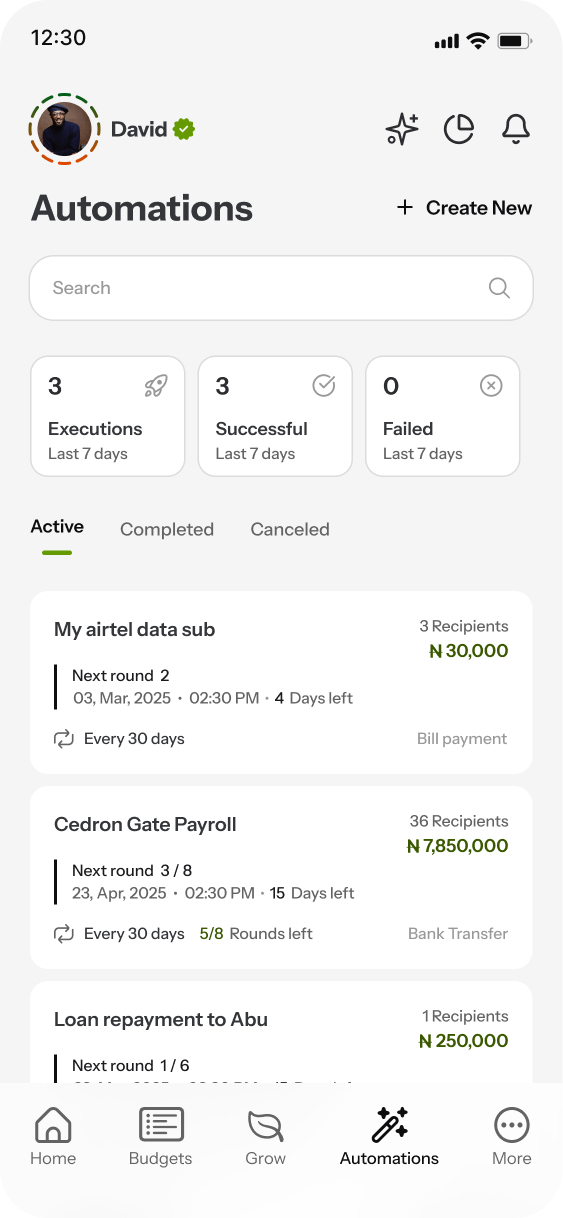

Recurring expenses (electricity, data, a regular family transfer) automate on their schedule regardless of when income arrived. The automation runs against the budget, not against incoming cash, so it doesn't create overdraft anxiety.

And because you spend from the app, every transaction is tracked from source. At any point, you know exactly what each budget has left. On a lean month, when the personal budget shows ₦5,000, you make choices accordingly. On a flush month, when it shows ₦45,000, you enjoy it without guilt, because the essentials and the buffer were funded first.

The Irregular Earner's Advantage

Here's something that rarely gets said: irregular earners who build this system often end up in a stronger financial position than salaried workers earning the same annual amount.

The reason is structural. Salaried workers expand their lifestyle to their paycheck because the paycheck is predictable; lifestyle inflation is invisible and continuous. Irregular earners who budget on their floor build a lifestyle below their average. The surplus accumulates. The buffer grows. The volatility that felt like a weakness becomes a forcing function for financial discipline.

The income is unpredictable. The spending doesn't have to be. Budget on your worst month. Let your best month build the future. That's not deprivation; it's the strategy that turns irregular income into irregular advantage.

Ready to take control of your money?

Download Delight Finance and create your first spendable budget in under 2 minutes.

Get Started — It's Free