How to Budget ₦200,000 in Lagos Without Going Broke

₦200,000 a month sounds like it should be enough. It's above minimum wage. It's a legitimate entry-to-mid-level salary in Lagos. And yet, by the 15th of most months, the account is already whispering.

We've seen this pattern in hundreds of Delight users earning between ₦150,000 and ₦250,000. The salary arrives on the 25th or 28th. By the first week, rent contributions, data, and a few meals out have taken a visible chunk. By the second week, transport and food are doing quiet damage. By week three, the balance is a number nobody wants to look at.

The instinct is always the same: I need to earn more. And yes, more income helps. But earning ₦300,000 without a system produces the same result at a higher altitude. The money still vanishes. The feeling is identical.

This is a different approach. Not a lecture on discipline. A real breakdown of where ₦200,000 actually goes in Lagos in 2026, and a plan that works with the numbers rather than against them.

Where the Money Actually Goes

Let's be specific. Here's what ₦200,000 faces in Lagos, assuming a single person sharing an apartment:

Rent contribution: ₦40,000 to ₦60,000. This is the monthly equivalent of an annual rent between ₦480,000 and ₦720,000, which is modest by mainland Lagos standards. If you're on the island, add another ₦20,000 to ₦40,000.

Transport: ₦20,000 to ₦35,000. If you're commuting from Ikorodu to the Island, or from Ajah to Ikeja, this is generous. Fuel prices in early 2026 have pushed BRT and Danfo fares up, and ride-hailing is a luxury at this salary. Budget for the commute you actually take, not the one you wish you took.

Food: ₦35,000 to ₦50,000. This assumes cooking most meals at home and buying from local markets. A pot of jollof rice that feeds you for two to three days runs about ₦4,000 to ₦5,000 in ingredients. Eating out, even buka-style, adds up fast: ₦1,500 to ₦2,500 per meal.

Electricity and data: ₦10,000 to ₦18,000. Prepaid meter or NEPA bill plus mobile data. If you work remotely and need reliable internet, data alone can hit ₦8,000 to ₦12,000.

Family obligations: ₦5,000 to ₦15,000. No Western budgeting model accounts for this, but in Nigeria it's not optional. A younger sibling's transport money. A contribution to a parent's medical bill. The ₦5,000 here, ₦10,000 there. It varies by month but it never hits zero.

Add those up. The low end: ₦110,000. The realistic middle: ₦145,000 to ₦160,000. That leaves ₦40,000 to ₦55,000 for everything else: savings, social life, haircuts, emergencies, the occasional treat that makes the month bearable.

That's the math. It's tight. And if there's no system guiding it, the ₦40,000 discretionary margin disappears into a fog of POS transactions that nobody can reconstruct at month's end.

The Real Problem Isn't the Amount

The common advice at this income level is to "cut expenses." But cut what? The rent you're already splitting? The transport to the job that pays you? The food? At ₦200,000, there isn't a luxury line item to slash. There's a margin to protect.

Protecting that margin is the entire game. And it requires one thing that spreadsheets and willpower can't provide on their own: a system where the allocation happens before the spending, not after.

A Budget-First Plan for ₦200,000

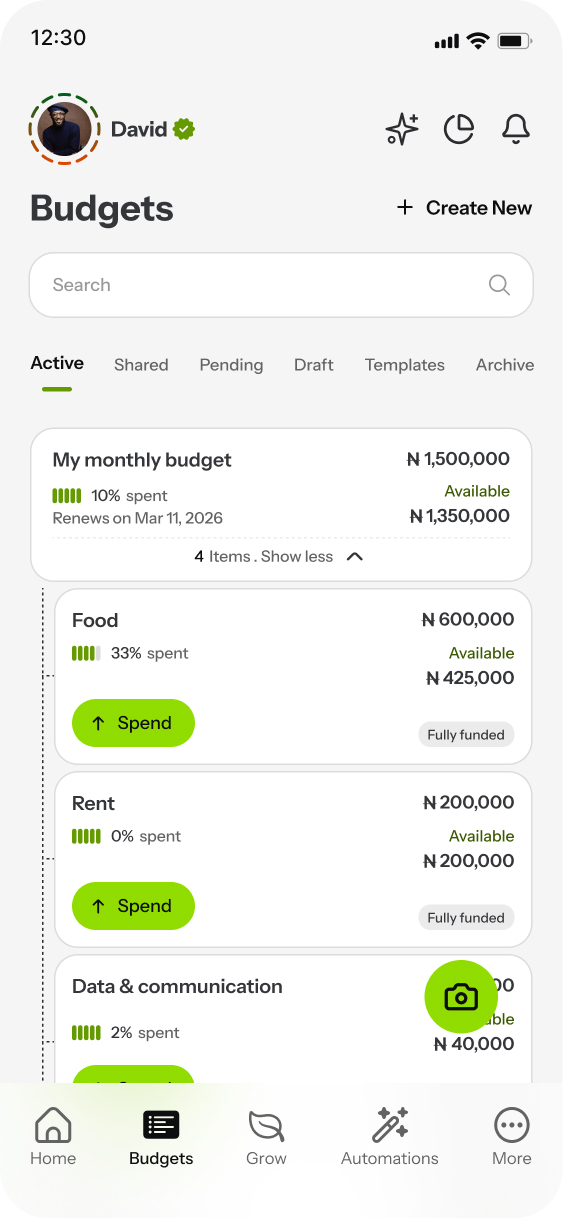

Here's how the same salary works under a budget-first approach. You create these budgets once. They persist and reset each month. The structure holds.

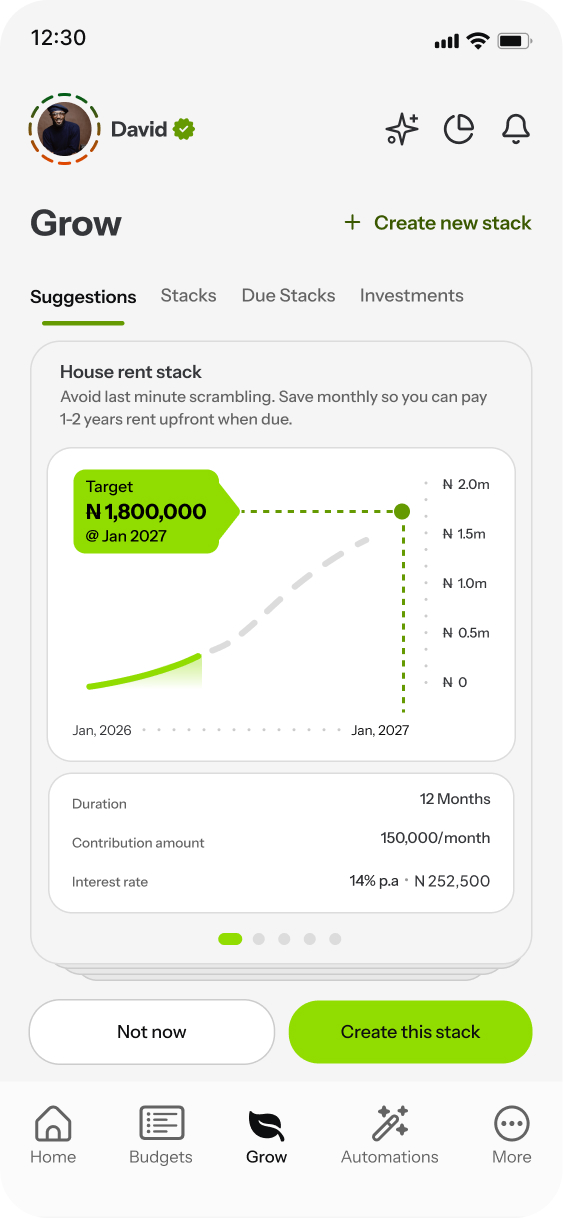

Rent Fund: ₦50,000. If your annual rent is ₦600,000, this builds the full amount in 12 months. Use a Stack to accumulate it. The money is visible, growing, and earmarked.

Food: ₦40,000. Based on what you actually spend, not a formula. If you cook at home five days a week and eat out twice, this covers it. If last month you spent ₦48,000, this is the number to interrogate, not guess at.

Transport: ₦25,000. Enough for the daily commute with a small buffer for unexpected trips.

Electricity & data: ₦14,000. Fixed enough to predict. Automate the payment so it leaves on the 1st without you thinking about it.

Family: ₦10,000. This month it's a sibling's textbooks. Next month it's a parent's prescription. The amount may shift; the budget should always exist.

Emergency buffer: ₦10,000. Not savings. A buffer for the things that aren't emergencies but aren't planned either: a colleague's contribution, a cab when the bus doesn't come, replacing a phone charger.

Savings (Stack): ₦15,000. Small but consistent. In a Stack, it accumulates. In 12 months, that's ₦180,000, almost a full month's salary set aside.

Personal: ₦36,000. Haircut. Data for streaming. A drink with friends on Friday. The line items that make life worth living at any income level.

Total: ₦200,000. Every naira assigned. No guessing.

What Changes Month to Month

The plan above isn't rigid. It's a starting point that flexes.

A friend's wedding comes up in March? That month, personal drops to ₦21,000 and ₦15,000 moves into a one-time "Wedding" budget for the aso-ebi and transport. The system doesn't break. The money moves visibly, intentionally, from one place to another.

Transport costs spike because of fuel prices in April? The transport budget adjusts to ₦30,000 and savings drops to ₦10,000 that month. Honest. Realistic. Not a failure of discipline.

The key is that every adjustment is a decision, not a discovery. You move the money before it's spent, not after it's gone.

Making It Automatic

The budget-first principle works on paper. But paper can't do what a system can.

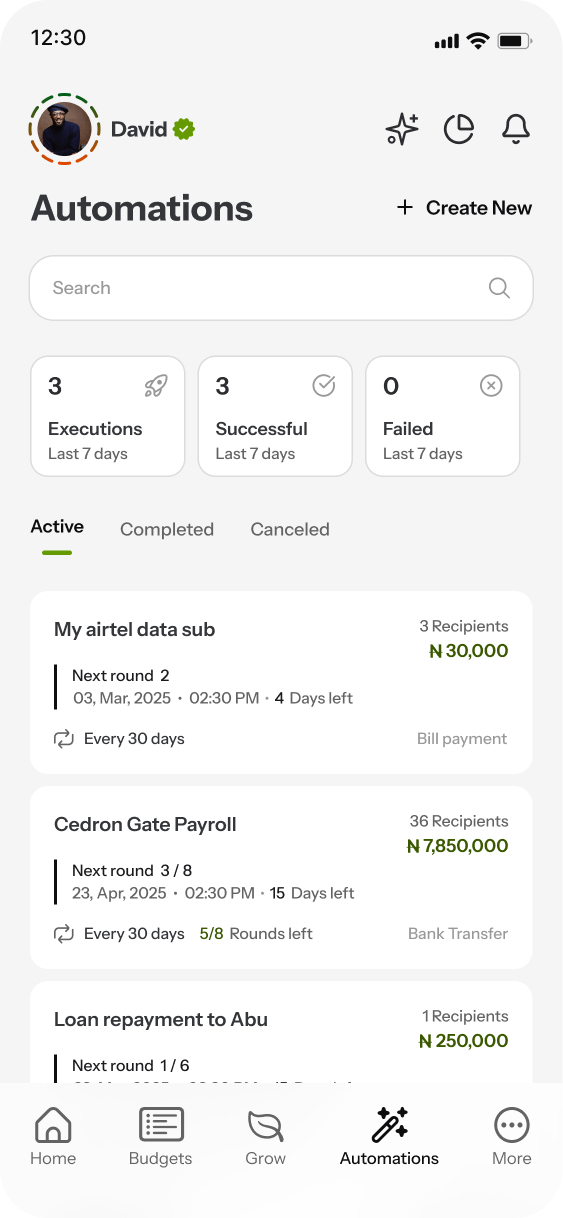

With Delight, you set up these budgets once and turn on autofunding. When your salary lands, the money distributes in the priority order you chose: rent first, food second, transport third, savings toward the end. You don't have to sit down and manually allocate. The system does what you already decided.

Your electricity bill? Automate it. Schedule the payment, set it to recur monthly, and it leaves the Electricity & Data budget on the 1st without you lifting a finger. The monthly ₦10,000 to your family? Same. Schedule it to one or multiple recipients, recurring, handled.

And because you spend directly from the app, every transaction is tracked from source. You don't log anything manually. At any point in the month, you can see that your food budget has ₦12,400 left, your transport has ₦7,200, and your personal fund is at ₦18,000. That visibility, before the purchase, not after, is what turns a tight salary into a manageable one.

The Honest Truth About ₦200K

We won't pretend ₦200,000 in Lagos is comfortable. It isn't. The margins are thin and the city doesn't care about your budget.

But there's a meaningful difference between ₦200,000 spent with intention and ₦200,000 that disappears without a trace. The first gives you clarity, small savings, and a sense of control. The second gives you the 15th-of-the-month anxiety that makes you question your entire career.

The salary isn't the problem. The absence of a plan for it is.

Set up the budgets. Let the system hold the structure. And if ₦200,000 truly isn't enough, if the math genuinely doesn't work after honest allocation, at least you'll know that with certainty, not with a vague feeling. That clarity is the first step to earning more, and keeping it.

Ready to take control of your money?

Download Delight Finance and create your first spendable budget in under 2 minutes.

Get Started — It's Free